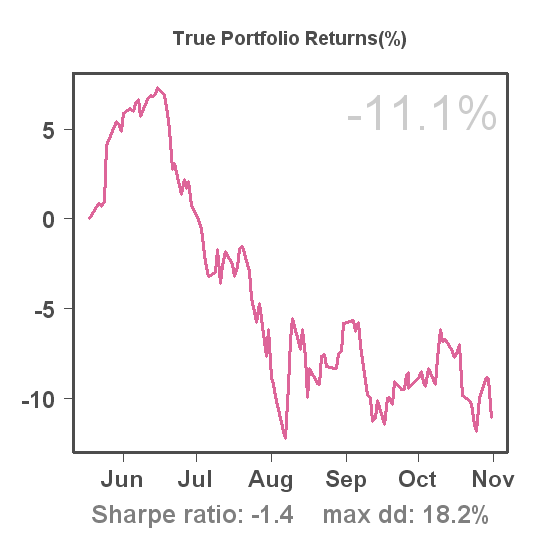

Please read the disclaimer at the bottom of this page

All positions have been adjusted to match the new portfolio weights. I also updated the hedge. I closed the previous DIA put (Sep '07 strike 123). The previous SPY put is pretty much worthless. The new hedge consists of some SPY Sep '07 puts with strike 144. If the SPY would drop by 6%, the delta should be app. equal to my portfolio beta of 1.6. Thus I'd expect to be about market-neutral below any 6% drop in the SPY. The reason for choosing 6% is that this is the largest drawdown for the SPY over the 1-year period for which I have data for all 3 systems in my portfolio.

Tomorrow is the last day of the month, a day on which I will implement the new portfolio weights. Because extreme-os positions are always open for one or two days at most, I don't have to change any of the actual positions. I can just change the auto trading settings on C2, such that the next trades are scaled properly.

For Weekend Trader and Trend Plays #1 it's a little different. They currently have open positions, which will probably stay open for quite a while. What I then do is simply adjust those positions such that they will reflect the new portfolio weights.

As I wrote earlier this week, the new weights will be:

extreme-os 127%

Weekend Trader 53%

Trend Plays #1 20%

I added a download section on the right-hand side. The first file available for download contains my real-life fills since March this year for extreme-os.

Taking the analysis in my previous post one step further, we can repeat it with the current performance of systems in the portfolio as inputs.

For example, Weekend Trader has a history of 404 trading days, and a Sharpe ratio of 1.68. What I want to know is: What happened to systems with an equal or longer history and a Sharpe ratio of at least 1.68 after they'd been around for 404 trading days?

It turns out 3 systems qualify: Mutual Fund Trader, extreme-os, and ARS.

These are their Sharpe ratios for the period starting after their first 404 trading days:

- Mutual Fund Trader 1.01

- extreme-os 4.01

- ARS 0.87

These odds are not really bad! (But remember that slippage and transaction cost are not accounted for)

We can repeat the same for Trend Plays #1. This system currently has a history of 241 trading days, and a Sharpe ratio of 2.40. Applying the same criteria to all other systems (including those that are terminated, of course), the following qualify: Mutual Fund Trader, extreme-os, vicinoo! trading - Daytrading, and Tango. Each of these had a Sharpe ratio > 2.40 over its first 241 trading days. How did they do afterwards?

- Mutual Fund Trader 1.01

- extreme-os 3.74

- vicinoo! trading - Daytrading 1.92

- Tango 2.14

Not bad either!

There's one big caveat to this kind of analysis: The underlying trend of the market was mostly upwards. If tomorrow a 3-year bear market would start, Sharpe ratios might not look very good for the next 3 years. One way around this would be to look at alphas instead of Sharpe ratios, which could be a good topic for future analysis.

The Sharpe ratio is often used as a measure of reward/risk and might be interesting as a criterion to select a system on C2. However, does past performance on the Sharpe ratio predict future performance? I'm not ready yet to show a rigorous analysis, but some preliminary findings might be interesting.

What I did a few weeks ago was to select all stock systems with at least a 1-year history (on C2). I then selected only those with a Sharpe ratio of at least 2 in the first year (250 trading days) since they appeared on C2. Finally, I calculated the Sharpe ratio over the period after the first year (not taking into account slippage and transaction cost). The underlying idea is: Suppose we would pick systems with Sharpe ratios > 2 and at least a 1 year history, how would they do afterwards.

The results are very interesting. I found 6 systems trading stocks with Sharpe ratio's >2 in their first year:

Mutual Fund Trader 2.25

extreme-os 4.53

vicinoo! trading - Daytrading 2.74

Tango 3.64

MBN-1 2.03

Weekend Trader 2.28

These are the Sharpe ratios I calculated for the period after the first year (note the length of this period is different per system, with the shortest being 89 trading days for MBN-1 and the longest being 399 days for Mutual Fund Trader):

Mutual Fund Trader 1.09

extreme-os 3.87

vicinoo! trading - Daytrading 2.48

Tango 2.03

MBN-1 -0.18

Weekend Trader 1.19

Interestingly, all Sharpe ratios in the second period are lower than in the first, but still very acceptable, except for one system: MBN-1. The ranking of systems is almost the same in both periods (except for Tango).

This seems to suggest that the Sharpe ratio has been quite informative for stock systems till so far. Of course, this is no guarantee that it will stay this informative in the future.

As I wrote yesterday, at the end of this month I will update the portfolio weights. The new weights will be:

extreme-os 127%

Weekend Trader 53%

Trend Plays #1 20%

Because Trend Plays has a shorter history and I just started trading this system, I am scaling in slowly. If it keeps performing well, I might increase to 30% by the end of June. There's now also a better balance between extreme-os and Weekend Trader.

What we gain from this change in portfolio weights is higher Sharpe and Sortino ratios.

Sharpe = 2.91 [0.91 , 4.88]

Sortino = 4.39 [1.22 , 8.35]

The downside is a portfolio with a higher beta and higher correlation with the general market.

Alpha (annualized) = 49%

Beta (SPY) = 1.29

Beta (DIA) = 0.35

R-squared = 0.38

N = 241 days

During the weekend I always run the following programs to keep my PC clean:

virus: AVG

spyware: Ad-Aware, AVG

registry: regvac

cache: ccleaner

McAfee and Defender are running on a daily basis, so in a way AVG should be redundant.

I also clean and defragment the HD, and check for any TradeBullet and TWS updates. Just installed TradeBullet build 527 and TWS build 872.6.